- Warmer weather and start of the World Cup created a boost in rapid delivery, which saw its highest share of online sales (12.8%) this year

- Promotional sales increased to 25% of FMCG purchases (up from 23.5%), with online rising to 29% as shoppers continued to prioritise value and convenience

- Online share of FMCG spend increases (+9.3%) while sales in the Convenience channel return to growth

Total Till sales at UK supermarkets rose (+4.6%) in the four weeks ending 13th June, improving from +4.2% in the previous period, reveals new data released today by NielsenIQ (NIQ). This was primarily driven by the end of May heatwave, when sales growth at the Grocery Multiples increased (+6.3%) in the two weeks ending 30th May, unit growth rose (+2.5%) and spend per visit was up (+2.3%).

However, NIQ data reveals that in the following two weeks to 13th June, sales growth slowed sharply (+0.4%), while unit growth fell (-1.7%), as cooler and wetter weather discouraged spending. Shoppers spent £490m less during these two weeks compared with the previous fortnight1. This is also reflected in consumer confidence remaining unchanged at -23, with shoppers continuing to hold a negative outlook on their personal circumstances.

Boost in promotional spending and online FMCG

In the four week period, promotional activity continued to play a key role in driving FMCG performance, with spend on promotion rising to 25% of total FMCG sales, up from 23.5% last year, which was helped by some new World Cup themed promotions. In the online channel, promotional spend was even higher (29%), as shoppers prioritised value for money and convenience of shop.

With this in mind, retailers increasingly relied on promotions, targeted price cuts and own label ranges to sustain demand, with own label sales (+5.4% value / +0.3% units) growing three times faster than branded sales. This was further supported by strong performance from premium own label lines, which recorded +9.1% value growth and +6.2% unit growth.2

With the uptick in sales and the start of the World Cup, the Convenience channel sales increased +1.7% year-on-year. Growth in convenience stores operated by the Grocery Multiples was also higher (+3.6%) compared with a year ago.

However, this growth remains well behind online share of FMCG spend, where sales increased (+9.3%) 2, making online the fastest growing channel in 2026. This was aided by the rise of rapid delivery which also benefited from the hottest day of the year so far, with rapid delivery reaching 12.8% share of online on 26th May 2026, its highest share of online sales this year to date 4.

Warmer weather also drove strong growth in outdoor and summer-led products, including suncare (+70%), prepared salad (+21% value) and fresh dips (+20% value). There was also growth in fresh foods (+4.4%), while frozen (+9.4%) became the fastest growing super category, driven by strong performance in ice cream (+34%) and frozen fruit (+28%), with total spend reaching £252m.

World Cup fever drives growth in drinks and world cuisine categories

There was also growth in the drinks categories, such as beer, wine and spirits (+2.7%), as well as soft drinks (11.9% value / +5.6% units). Shoppers also spent £411m on lager, where sales rose (+7.9%), and £111m on cider (+10%). Premix alcoholic drinks (+51%) also saw strong growth. This coincides with the start of the World Cup and warmer weather, encouraging consumers to host viewing parties and social occasions.

The impact of The World Cup was also reflected in the demand for new cuisines and world flavours, with the cooking sauces category showing heightened consumer interest in experimenting with more diverse foods. Interest was particularly strong in Japanese (+9.0%)4, Thai & South East Asian (+14.8%), Spanish (+31.2%) and Mexican (+7.1%) flavours. In contrast, unit growth across more mainstream cuisines declined, including British (-0.9%) and Indian (-2.4%), while Italian recorded modest growth (+0.7%).5

NIQ data shows that 43%6 of shoppers now experiment with new recipes and cuisines at least every fortnight, a trend that is prompting retailers and brands to expand world-inspired ranges to capitalise on growing consumer appetite, further amplified by global events such as the World Cup.

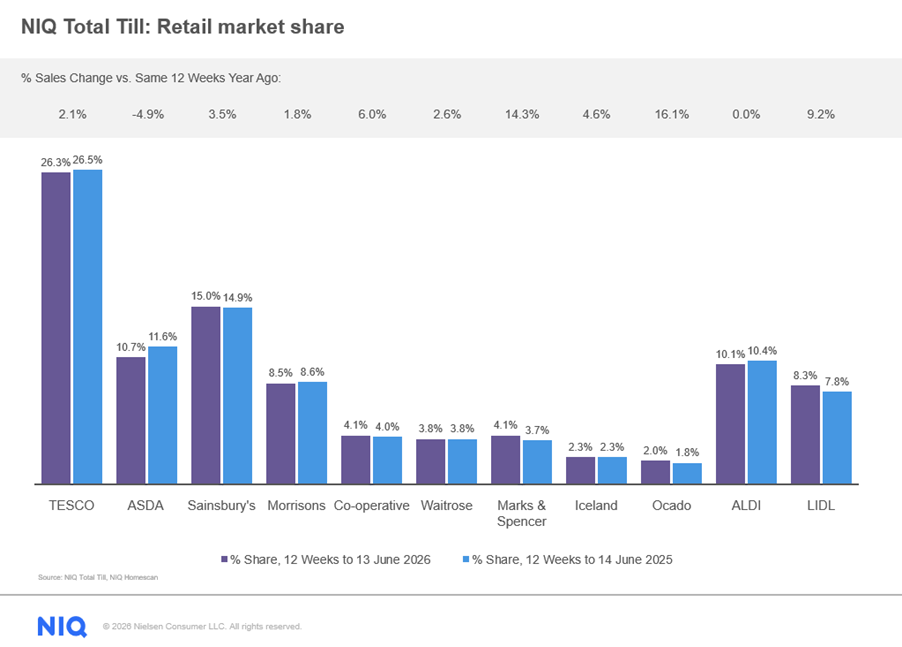

Over the 12 weeks, Asda was the only major retailer to see sales decline (-4.9%). Ocado was the fastest growing retailer (+16.1%), followed by M&S (+14.3%) and Lidl (+9.2%). Co-op sales also increased (+6.0%) alongside Sainsbury’s (+3.5%), which continued to grow market share and rose to 15.0%. In contrast, Aldi sales were flat at 0.0%.

Mike Watkins, Head of Retailer and Business Insight at NielsenIQ, says: “The arrival of hot weather boosted demand for summer essentials, with suncare, ice cream and refreshment related categories among the fastest growing areas of grocery spend. As well as outdoor dining occasions, dips and sharing foods as consumers made the most of the early summer weather and retailers adapted ranges to meet this demand.”

Watkins adds: “Looking ahead, the second heatwave of the year will likely see another boost to sales into July, conveniently coinciding with the summer of sport. Yet, we still expect lower demand into August when the holiday season disrupts spending. The economic outlook for September is still uncertain with increases in mortgage and energy costs expected and the possibility that accelerating food inflation could start to take a bigger share of disposable incomes, which may add further uncertainty for households. Retailers and brands will therefore need to continue to find innovative ways to encourage shoppers to spend to maintain the current sales momentum.”

1NIQ Scantrack Total Coverage

2Homescan FMCG 12 we 13.06.26

3NIQ Scantrack Defined Grocery Multiples e commerce 4 w.e 13th June 2026

4 NIQ Digital Purchases Value Share | YTD is up to 13th June 2026

5NIQ Scantrack | Total Coverage | 12 weeks to 13.06.26

6 NIQ Homescan Survey | November 2025

Comments are closed.